Nassau Tobacco: Everyone Knew It Was Dying. Nobody Knew When.

Can AI Predict Municipal Defaults? Nassau Tobacco Just Became the Test Case.

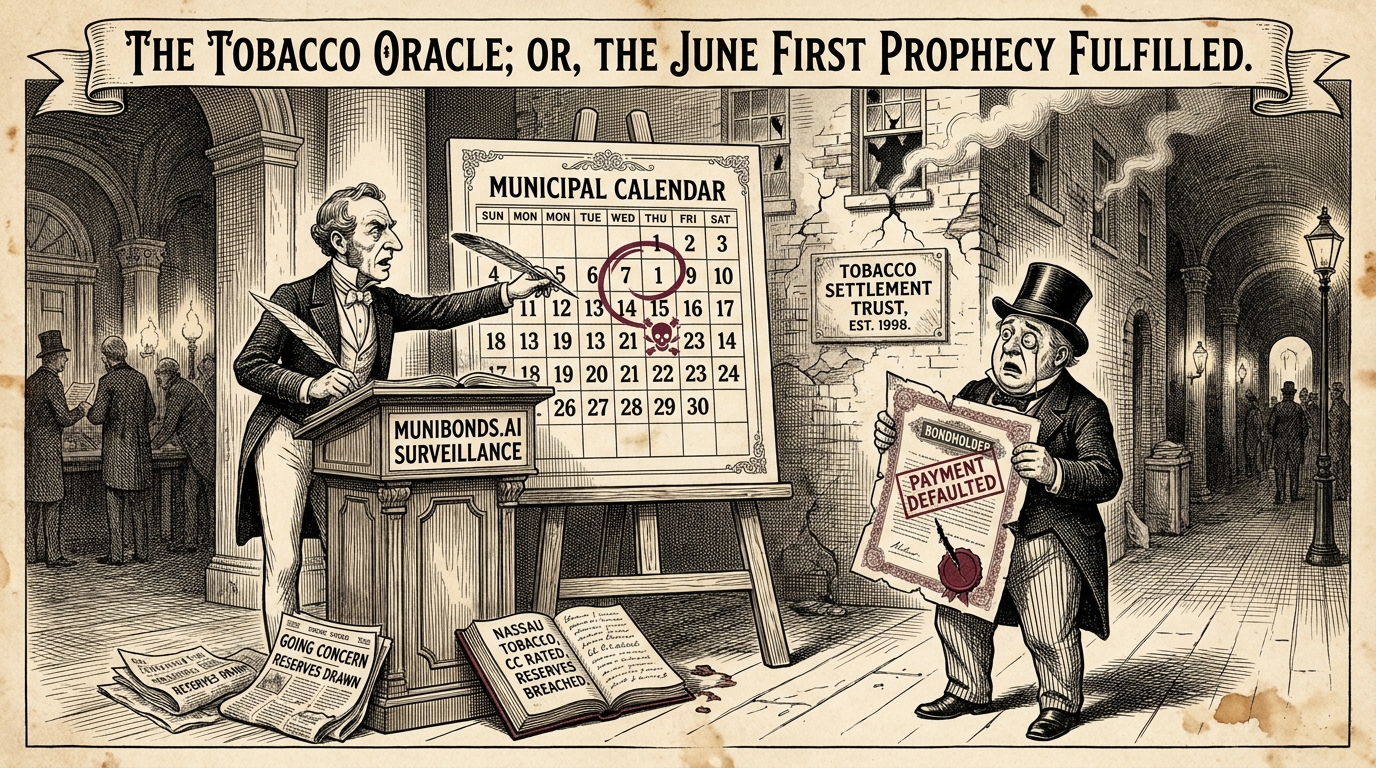

On March 18, MuniBonds.ai issued a warning that was unusually specific.

The platform assigned Nassau County Tobacco Settlement Corporation its lowest AI Credit Sentiment rating and identified a single event—the June 1 debt payment—as the most likely point of failure. Two and a half months later, that payment was missed.

For decades, municipal credit analysis has operated under a simple assumption: defaults are rare, difficult to predict, and often understood only in hindsight. Investors, analysts, and rating agencies spend enormous amounts of time identifying troubled credits. The harder question is determining when a troubled credit becomes a defaulting one.

Nassau Tobacco may have just provided the first real-world test of whether artificial intelligence can answer that question.

The June 1 payment default marked what industry participants identify as the first payment default in the history of the $80 billion municipal tobacco bond market. But the more consequential story may not be the default itself. It may be the fact that an AI-powered surveillance system identified the likely failure point months before it occurred.

The distinction matters.

The market did not need artificial intelligence to know Nassau Tobacco was distressed. Investors had watched tobacco settlement revenues decline for years. Reserve funds had been drawn repeatedly. Auditors had raised going-concern concerns. S&P had downgraded the credit to CC. Bond prices had been falling steadily as investors reassessed the probability of repayment.

The risk was visible. The timing was not. That is where MuniBonds.ai enters the story.

Rather than attempting to predict the future from a single data point, the platform continuously monitors thousands of municipal issuers, combining financial disclosures, audited statements, rating actions, reserve activity, market behavior, news events, and structural credit characteristics into a unified surveillance framework. The objective is not simply to identify distressed credits. It is to determine when a deteriorating credit has crossed a threshold where default becomes a probable outcome rather than a theoretical risk.

In Nassau Tobacco’s case, the system concluded that threshold had been crossed.

The March 18 report cited a decade of reserve fund deterioration, a breached liquidity reserve, a going-concern audit opinion, a CC rating from S&P, and a looming debt-service obligation that significantly exceeded expected settlement revenues. Viewed individually, none of these signals were new. Viewed collectively, they painted a different picture. The credit was no longer merely weak. It was running out of time.

The prediction was clear enough to be tested. A specific issuer. A specific obligation. A specific anticipated failure point. And ultimately, a specific outcome.

That is unusually rare in municipal finance, where many risks play out over years and where outcomes are often open to interpretation. Nassau provided something closer to a controlled experiment. The warning was issued. The date was identified. The payment was missed.

Whether this proves that AI can predict municipal defaults is a larger question that will require many more observations, many more credits, and many more market cycles.

One correct prediction does not establish a track record.

But it does establish something important: the hypothesis can be tested.

For years, artificial intelligence has promised to transform investment research, credit analysis, and risk management. Much of that promise has remained theoretical. Nassau Tobacco changed that. For perhaps the first time in the municipal market, an AI-generated credit warning was followed by a measurable, real-world default event that aligned with the system’s assessment.

That makes Nassau more than a tobacco bond story. It makes it a case study.

If municipal defaults are not random events but the end result of identifiable patterns hidden within enormous volumes of public information, then the future of credit surveillance may belong to systems capable of finding those patterns faster, more consistently, and with greater discipline than any human analyst can.

Nassau Tobacco may not be remembered as the first tobacco bond default. It may be remembered as the moment municipal investors began asking a different question:

Can AI predict municipal defaults?

And for the first time, there is evidence that the answer might be yes.