Nassau Tobacco: The First Real Test of AI in Muni Defaults

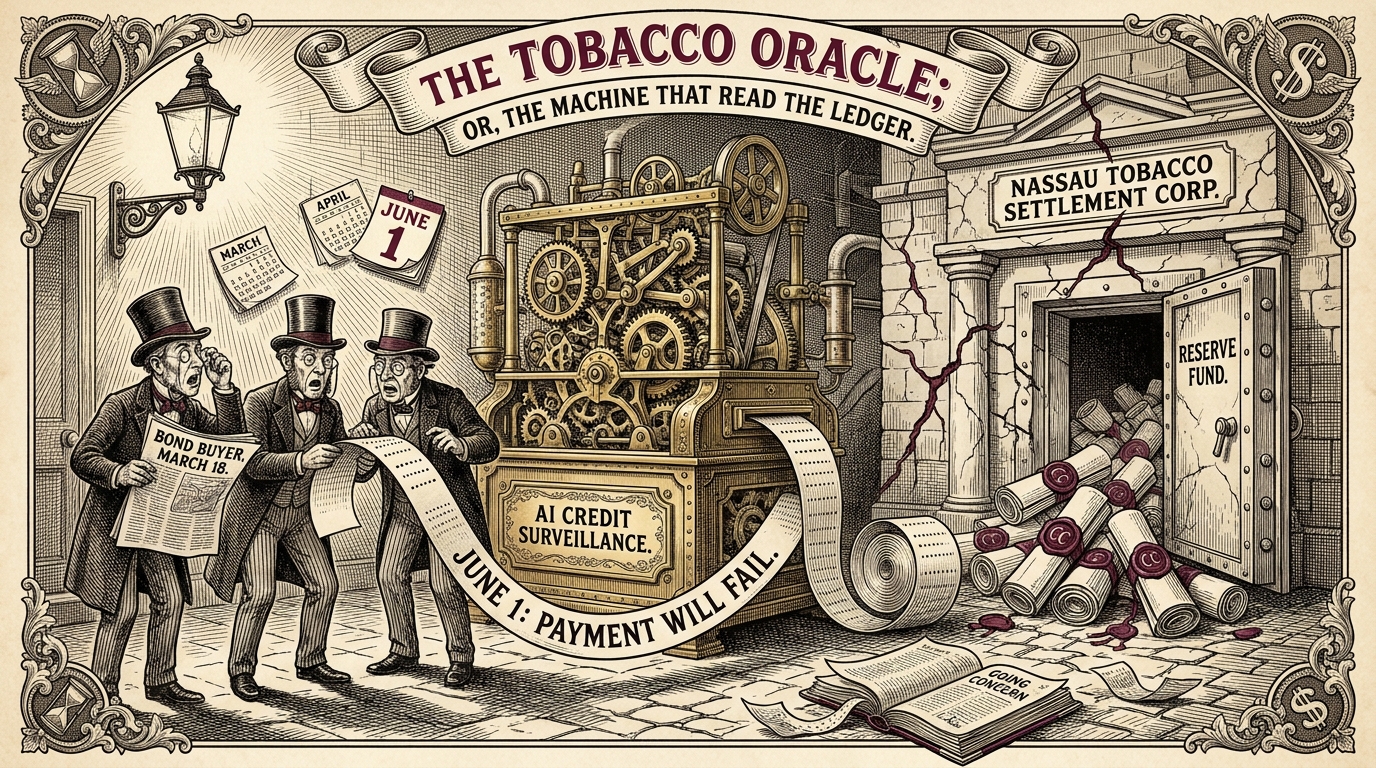

On March 18, MuniBonds.ai issued a warning about Nassau County Tobacco Settlement Corporation that was unusually specific. The platform assigned the issuer its lowest AI Credit Sentiment rating and identified a single event, the June 1 debt payment, as the most likely point of failure (MuniBonds.ai research note, March 18 2026). Two and a half months later, that payment was missed (EMMA material event notice, June 1 2026).

For decades, municipal credit analysis has operated under a simple assumption: defaults are rare, hard to predict, and usually understood only in hindsight. Investors, analysts, and rating agencies spend enormous time identifying troubled credits. The harder question has always been figuring out when a troubled credit becomes a defaulting one. Nassau Tobacco may have just provided the first real-world test of whether AI can answer that question.

The first payment default in an $80 billion market

The June 1 miss marks what industry participants identify as the first payment default in the history of the roughly $80 billion municipal tobacco bond market (Bond Buyer, June 2026). That alone is a market-structure event worth recording. Tobacco settlement bonds have been a quiet workhorse of the muni market since the 1998 Master Settlement Agreement, and they have absorbed two decades of declining cigarette consumption without a single payment failure.

But the more consequential story may not be the default itself. It may be that an AI surveillance system flagged the likely failure point months before it happened.

The risk was visible. The timing was not.

The market did not need AI to know Nassau Tobacco was distressed. Investors had watched tobacco settlement revenues decline for years. Reserve funds had been drawn repeatedly. Auditors had raised going-concern concerns. S&P had downgraded the credit to CC (S&P Global Ratings, 2025). Bond prices had been falling as investors reassessed the probability of repayment.

The risk was visible. The timing was not. That gap, between knowing a credit is weak and knowing when it will fail, is where most municipal analysis runs out of room.

What the platform actually did

Rather than try to predict the future from a single data point, MuniBonds.ai continuously monitors thousands of municipal issuers. The platform combines financial disclosures, audited statements, rating actions, reserve activity, market behavior, news events, and structural credit characteristics into one surveillance framework. The objective is not just to identify distressed credits. It is to determine when a deteriorating credit has crossed the threshold where default becomes a probable outcome rather than a theoretical risk.

In Nassau’s case, the system concluded that threshold had been crossed. The March 18 report cited a decade of reserve fund deterioration, a breached liquidity reserve, a going-concern audit opinion, the CC rating from S&P, and a looming debt-service obligation that significantly exceeded expected settlement revenues (MuniBonds.ai research note, March 18 2026). Viewed individually, none of these signals were new. Viewed collectively, they painted a different picture. The credit was no longer merely weak. It was running out of time.

A prediction clear enough to be tested

The prediction was clear enough to be tested. A specific issuer. A specific obligation. A specific anticipated failure point. And ultimately, a specific outcome. That is unusually rare in municipal finance, where many risks play out over years and where outcomes are often open to interpretation.

Nassau provided something closer to a controlled experiment. The warning was issued. The date was identified. The payment was missed.

What one prediction does and does not prove

Whether this proves AI can predict municipal defaults is a larger question that will require many more observations, many more credits, and many more market cycles. One correct prediction does not establish a track record. It is not like we are able to do something magical that nobody else can. The signals were public. The audit was public. The rating was public. What the system did was assemble them into a single read on a single date.

But it does establish something important: the hypothesis can be tested. For years, AI has promised to transform credit analysis. Much of that promise has stayed theoretical. Nassau Tobacco changed that. For perhaps the first time in the muni market, an AI-generated credit warning was followed by a measurable, real-world default event that aligned with the system’s assessment.

Why this matters beyond tobacco

If municipal defaults are not random events but the end result of identifiable patterns hidden inside enormous volumes of public information, then the future of credit surveillance may belong to systems that can find those patterns faster and more consistently than any human analyst working alone. The muni market has nearly two million bond issues worth about $3.7 trillion in total (SIFMA, 2026). Each issuer carries thousands of pages of disclosure. No analyst desk reads all of it. A surveillance layer that does is a different kind of tool than a rating.

Nassau Tobacco may not be remembered as the first tobacco bond default. It may be remembered as the moment municipal investors began asking a different question: can AI predict municipal defaults? For the first time, there is one data point suggesting the answer might be yes.

It is early days. If you manage a portfolio with exposure to tobacco settlement paper or other sectors where reserve draws and going-concern language have started showing up in audits, the question is whether the same pattern recognition can be run across your holdings before the next payment date arrives. That is the surveillance layer MuniBonds.ai runs across the disclosure stack. Worth a look if you are covering hundreds of credits and the auditor questions are getting harder to answer.