The Subterranean Fault Line Under Higher Ed

Higher education bonds are showing cracks beneath the surface.

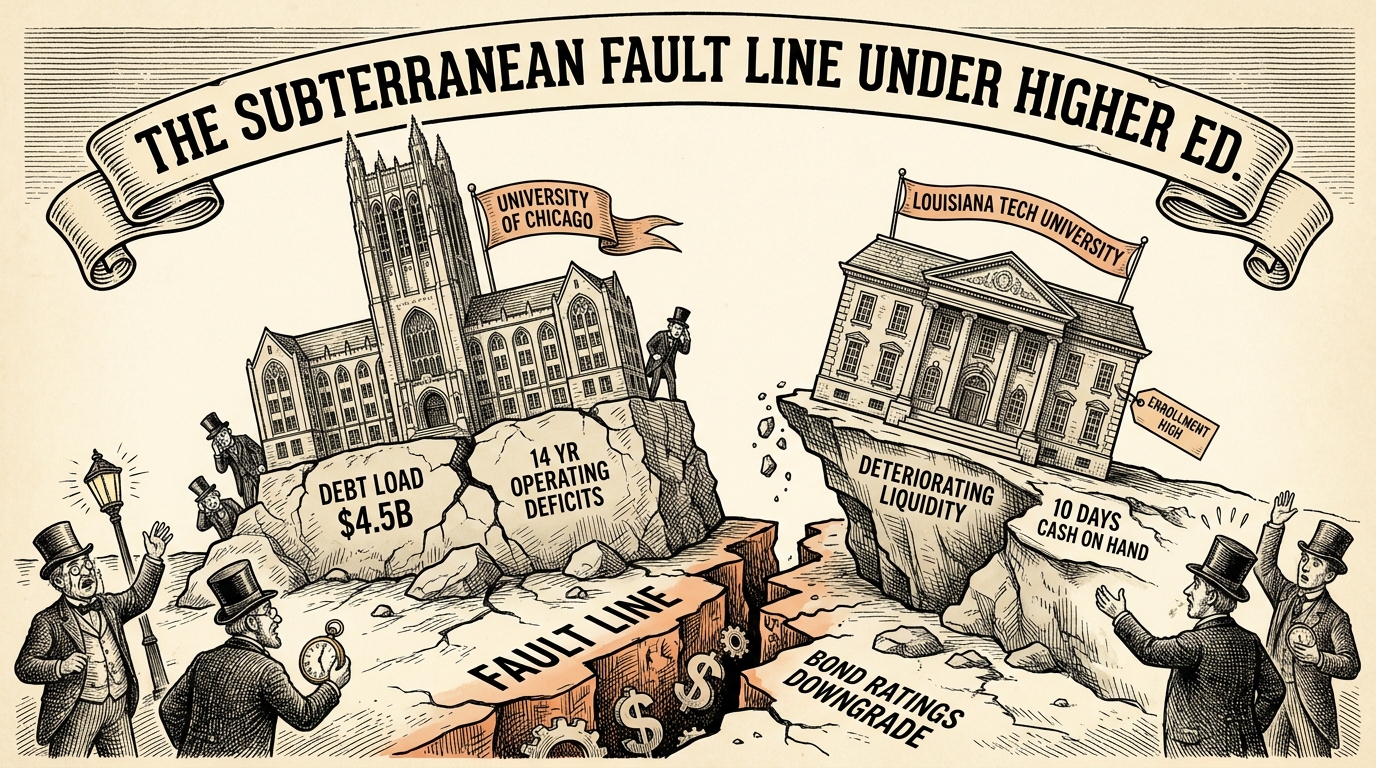

Something is quietly failing in the seemingly safe world of higher education. While the protagonist of our initial concern might be Louisiana Tech University, its struggles, when paired with data from elite institutions, reveal a system in trouble. And if you listen to the numbers, you’ll hear something quite unnerving for investors in university of chicago bonds and other higher education debt.

Just at the moment when Louisiana Tech’s enrollment hits a high — 12,145 this fall, its largest freshman class ever — the institution’s lifeline is slipping. Moody’s has downgraded the school’s issuer rating two notches to Baa2, citing “deteriorating liquidity” and projecting just about 10 days of cash on hand for fiscal 2025. The image is stark: a university running day-to-day in a world built for decades.

It doesn’t stop there. In parallel, at the elite end of the market, the University of Chicago is laying bare a different, yet related, set of warning signs. According to MuniBonds.ai’s blog post, Chicago carries roughly $4.5 billion in outstanding bond debt, has run operating deficits for 14 consecutive years, and sports a debt-to-asset ratio of 68% – more than double any peer institution.

Here’s the central insight: this isn’t about one school making a bad decision. It’s about an entire sector that borrowed, built, and expanded on assumptions that are unraveling.

Key Takeaways: Understanding the Financial Stress in Higher Ed

This post analyzes the hidden financial challenges facing the higher education sector, highlighting specific concerns for municipal bond investors, particularly those holding university of chicago bonds.

- Dual Crisis: While Louisiana Tech faces a liquidity crisis (10 days cash on hand), the University of Chicago reveals deep structural issues despite its prestige.

- University of Chicago’s Red Flags: $4.5 billion in bond debt, 14 consecutive years of operating deficits, and a 68% debt-to-asset ratio (double its peers).

- Sector-Wide Problem: These aren’t isolated incidents but symptoms of an entire sector struggling with outdated business models, rising costs, and shifting demographics.

- Investor Action: Investors in higher education muni bonds must look beyond prestige and ratings, focusing on liquidity, debt service, and enrollment trends.

> Read the Full In-Depth Research Report

A Dual Narrative: Louisiana Tech Meets Chicago

The current landscape of higher education finance presents a stark dual narrative.

Louisiana Tech University: Under-the-Radar Strain

At Louisiana Tech, the narrative is one of under-the-radar strain. The school’s liquidity has been shrinking, state support has stagnated, expenses have surged, and yet it pressed on, buoyed by rising enrollment. It looked like growth, but underneath the veneer, the cash cushion had vanished. The downgrade is the moment the façade cracks.

University of Chicago: The Loudest Warning for “Elite” Bonds

At the University of Chicago, the story is louder and, for investors in university of chicago bonds, harder to ignore. An institution whose prestige is unquestioned is now revealing that even a stellar reputation is no shield against financial stress. The blog piece details:

- Cumulative Deficits: 14 consecutive years of operating deficits.

- High Leverage: An aggressive debt-to-asset ratio of 68%.

- Aggressive Borrowing: Substantial borrowing for new facilities.

- Fragile Assumptions: Reliance on assumptions about endowment returns, research funding, and student demand that are becoming increasingly fragile.

Both institutions are operating in a world where the external environment is shifting faster than traditional business models can adjust, impacting their financial stability and the risk profile of their municipal bonds.

The Anatomy of the Problem

Let’s pull apart what’s really going on across the higher education sector, impacting both small regional universities and major research powerhouses like the University of Chicago:

- Liquidity Mirage: Louisiana Tech’s “10 days of cash” suggests an institution living dangerously close to the edge.

- Leverage and Debt: University of Chicago’s 68% debt-to-asset ratio signals a heavy reliance on borrowing.

- Chasing Growth: Universities built for expansion now face shrinking demographics and rising costs.

- Federal Funding Exposure: Chicago depends heavily on federal research dollars and student aid.

- Deferred Maintenance: The sector-wide backlog is estimated at $950 billion, a future liability disguised as a current non-event.

- Ratings Lag Reality: Chicago retains strong ratings despite years of deficits — a mismatch that should make investors uneasy.

- Structural Shifts: Fewer college-age students, fewer adult learners, higher operating costs, and rising competition create systemic strain.

Why This Matters for Municipal Bond Investors

The higher-ed sector holds about $262 billion in outstanding muni debt. While diversification looks strong on paper, many institutions share these same underlying weaknesses. The University of Chicago’s bond crisis warning signs, outlined in our previous blog, show how even top-tier institutions can mask severe financial stress that can impact bond performance.

Key metrics investors must monitor:

- Years of operating deficits

- Debt service as a share of expenses

- Liquidity and days cash on hand

- Exposure to federal funding

- Enrollment trends and selectivity

- Deferred maintenance obligations

- Market signals like spread widening

As the article notes, a prestigious name or large endowment is not a guarantee of financial resilience when evaluating university of chicago bonds or any higher education debt.

A Narrative of Choices and Consequences in Higher Education Finance

You can imagine two university boardrooms facing the same future. One assumes growth will continue: more students, more research funding, higher tuition. The other assumes the opposite: fewer students, tighter budgets, higher capital needs. The former borrows; the latter retrenches.

University of Chicago exemplifies the long-run effects of choosing expansion and leverage. Louisiana Tech represents the quieter institutions that appear steady until liquidity metrics reveal the true picture. In both cases, the numbers tell a story of institutions misaligned with the realities unfolding around them.

Tying It Back to the Broader Market

Higher education is changing faster than many institutions, and many investors, anticipated. When even high-prestige universities are showing structural financial stress, the question becomes not if more trouble is coming, but where it appears next.

The University of Chicago exemplifies the long-run effects of choosing aggressive expansion and leverage. Louisiana Tech represents the quieter institutions that appear steady until liquidity metrics reveal the true picture. In both cases, the numbers tell a story of institutions misaligned with the realities unfolding around them.

Final Thought

The stories of Louisiana Tech and the University of Chicago are not anomalies; they’re signals. They reveal a sector whose old assumptions no longer match its new realities.

For municipal bond investors, relying on names, endowments, or outdated credit ratings isn’t enough. You need real-time data—liquidity trends, debt ratios, enrollment patterns—the early indicators that separate resilience from risk, especially when evaluating university of chicago bonds.

Because in higher education, the story is changing. The question is whether investors notice before the next chapter arrives.

Frequently Asked Questions (FAQ) about University of Chicago Bonds & Higher Ed Finance

Q: What are the key financial concerns for the University of Chicago? A: The University of Chicago has $4.5 billion in outstanding bond debt, has reported operating deficits for 14 consecutive years, and has a high debt-to-asset ratio of 68%, significantly higher than its peers.

Q: How do University of Chicago bonds compare to Louisiana Tech’s situation? A: While Louisiana Tech faces an immediate liquidity crisis (only 10 days cash on hand), the University of Chicago’s issues are more structural—high leverage and consistent operating deficits—indicating long-term financial strain despite its prestige.

Q: Does a strong reputation protect university bonds? A: As the University of Chicago’s situation shows, a strong reputation and large endowment are not a guarantee of financial resilience. Investors need to look at underlying financial metrics like liquidity, debt ratios, and operating performance.

Q: What is a “debt-to-asset ratio” and why is 68% high? A: The debt-to-asset ratio measures how much of a university’s assets are financed by debt. A 68% ratio means 68% of Chicago’s assets are funded by borrowing, which is considered very high and indicates significant financial leverage.

Q: What should muni bond investors look for in higher education debt? A: Investors should scrutinize operating deficits, debt service burdens, days cash on hand (liquidity), exposure to federal funding, enrollment trends, and deferred maintenance obligations, rather than relying solely on credit ratings or institutional prestige.

About MuniBonds.ai

MuniBonds.ai provides advanced credit analytics and risk-monitoring tools for municipal bond investors. We believe in separating speculation from smart investing by seeing past the name and into the true risk profile of higher education credits.

For a deeper dive into the University of Chicago’s financial specifics, revisit our original analysis: University of Chicago Bond Crisis: Warning Signs for Municipal Bond Investors