ICE CAPADES! $83M Hockey Palace Had $18 in the Bank When the Bill Came Due

ICE CAPADES!

$83M Hockey Palace Had $18 in the Bank When the Bill Came Due

MuniBonds.ai • March 29, 2026

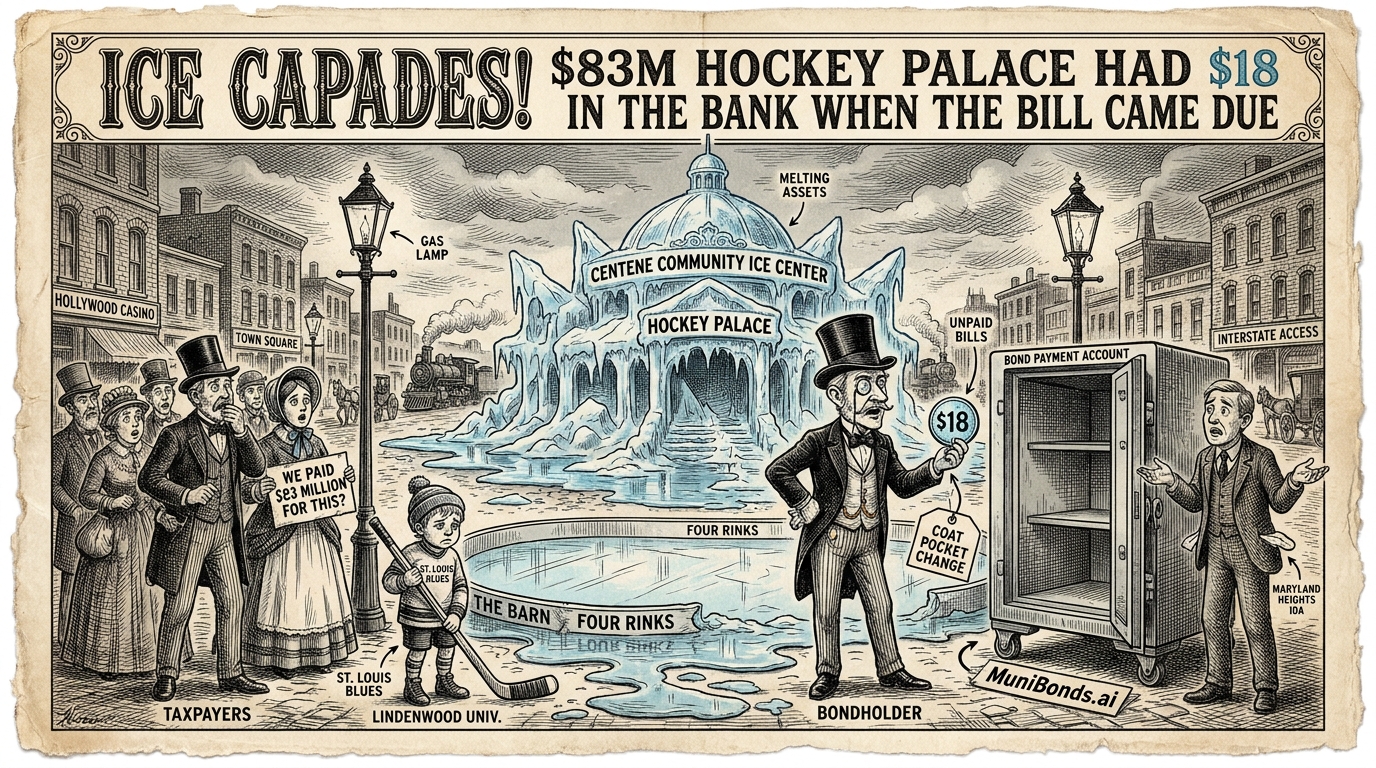

Here is a number that tells you everything you need to know about the most striking stadium bond default of the year, at the Centene Community Ice Center in Maryland Heights, Missouri: eighteen dollars.

That was the balance in the bond payment account when the bill came due. Eighteen dollars. Not eighteen thousand. Not eighteen million. Eighteen. The kind of money you might find in a coat pocket. The kind of money that buys you a sandwich and a coffee, but not, as it turns out, the debt service on $50.2 million in revenue bonds backing a four-rink hockey palace on the outskirts of St. Louis.

A Stadium Bond Default in Slow Motion

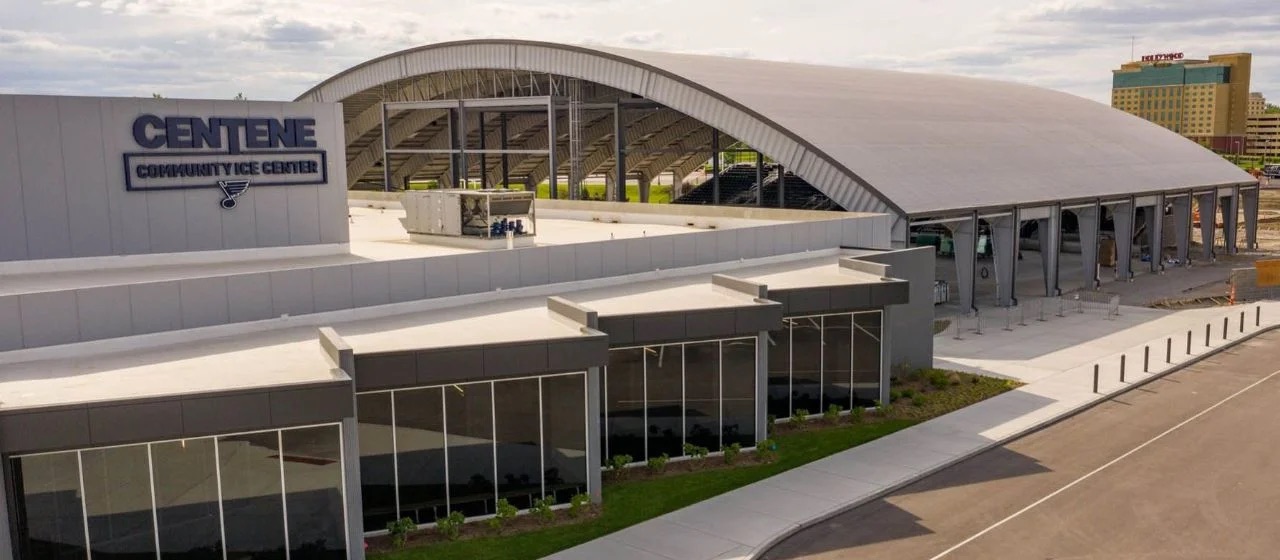

The Centene Community Ice Center was supposed to be different. It was supposed to be the thing that put Maryland Heights—a quiet suburb wedged between a Hollywood Casino and an interstate—on the map. Four NHL-sized rinks. A 2,500-seat arena with an HD scoreboard. A covered outdoor rink called “The Barn” with grandstand seating for 4,000. The practice home of the St. Louis Blues. The home ice of Lindenwood University’s newly minted NCAA Division I hockey program. A destination for tournaments, figure skating competitions, and weekend birthday parties. Total price tag: $83 million.

On March 15, 2026, the Maryland Heights Industrial Development Authority couldn’t make its bond payment. It drew down the reserve fund to cover the senior debt. It couldn’t cover the subordinate debt at all. The revenue fund balance was zero. And the people who had lent $55.7 million to make this dream a reality were left holding the bag.

The Centene Community Ice Center is a cautionary tale about what happens when a community bets its credit rating on a building that can’t pay for itself — a textbook stadium bond default unfolding in slow motion. Read our report here. The Maryland Heights Hockey Rink Bond Collapse or listen to the Pod Cast:

The Promise

To understand how this happened, you have to go back to 2018, when the ice center was still a set of architectural renderings and a very compelling PowerPoint presentation. The pitch went something like this: the St. Louis Blues—fresh off their first Stanley Cup in franchise history the following year—needed a world-class practice facility. Maryland Heights needed an economic engine. A nonprofit called the St. Louis Legacy Ice Foundation, led by current and former Blues executives, would raise $15 million in private money. The city would issue the bonds—$50.2 million in senior Series 2018A revenue bonds, and another $5.5 million in subordinate Series 2018B bonds—to cover the rest.

The structure was elegant, or at least it looked elegant on paper. Maryland Heights would own the building. The Legacy Ice Foundation would lease it for 30 years. Lease payments, combined with arena revenues, would service the debt. Projections called for $20 million a year in revenue. Everybody would win. The Blues get a palace. Lindenwood gets a home rink. Local kids get ice time. Bondholders get their coupon. And Maryland Heights gets to be famous for something other than its proximity to a casino.

These bonds carried no rating. This is worth pausing on. When a bond is unrated, it means that none of the major credit agencies—not S&P, not Moody’s, not Fitch—have examined the deal and put their stamp on it. It means that investors who bought these bonds were, in effect, doing their own homework. Or, more likely, trusting that someone else had done it for them.

The Pandemic and the Crack-Up

The Centene Community Ice Center opened its doors in September 2019. Six months later, a novel coronavirus shut down the world. If you were writing a screenplay about the worst possible timing for opening a large indoor public gathering space, you could not improve on this.

The rink closed. The tournaments didn’t come. The birthday parties stopped. And when the facility finally reopened, the crowds never reached the numbers that the spreadsheets had promised. The $20 million in projected annual revenue turned out to be a fiction—the kind of projection that looks reasonable in a conference room but evaporates on contact with reality.

Then things got worse. In 2021, the general contractor filed a mechanics lien against the nonprofit operator. The parties settled the lawsuit in 2022 on confidential terms—which, in the world of municipal finance, is a polite way of saying money changed hands and nobody can tell you how much. Then it emerged that the ice center had failed to collect sales tax for four straight years—a $1.5 million error that happened because, apparently, a city employee told the operators they didn’t need to charge sales tax since the building was publicly owned. This was incorrect.

When a revenue bond fails, it doesn’t fail like a stock. It fails slowly, then all at once—one missed payment, one reserve draw, one material event notice at a time.

The Two Classes of Losers

Here is the part of every stadium bond default story that matters most to anyone holding a municipal bond, and it’s the part that almost never gets explained clearly: not all bondholders are equal. In fact, the architects designed this deal so that when things went wrong—and things always go wrong—some people would lose their money before other people lost theirs.

The Series 2018A bonds were the senior debt. They had first claim on revenues. They had a debt service reserve fund—a rainy-day account required to hold $3.12 million at all times. When the March 15 payment came due and the revenue fund was empty, the trustee reached into that reserve and pulled out enough to cover the principal. It wasn’t pretty. It was an “unscheduled draw,” which in bond language is the equivalent of breaking the glass on a fire extinguisher. But the senior bondholders got paid.

The Series 2018B bondholders were not so lucky. They held subordinate debt—second in line, behind the senior bonds, behind the reserve fund, behind everyone. When the money ran out, their March 15 interest payment was only partially satisfied. A “restricted contribution” arrived on March 11—four days before the deadline—but it wasn’t enough. The 2018B bonds are now in formal default.

This is subordination risk, and it’s not theoretical. It’s the difference between getting paid and getting a letter from a trustee explaining why you didn’t. The people who bought the 2018A bonds and the people who bought the 2018B bonds were betting on the same hockey rink. They were watching the same games. But they were not in the same seats.

Credit Rating Carnage After a Stadium Bond Default

Maryland Heights has suffered extraordinary damage. In March 2021, S&P Global Ratings downgraded the city from AA-minus to BBB-plus—a fall from near the top of the investment-grade ladder to a few rungs above junk. The reason: the ice rink. In October 2022, after the city forwarded funds to cover a delinquent bond payment, S&P cut again—BBB-minus for the city, BB-plus for its certificates of participation. BB-plus is junk. The rating agency cited “the city’s unwillingness to support the bonds” as a “risk management, culture, and oversight weakness.”

Think about what that means. A city that was once rated AA-minus—a rating that says, essentially, “this is a very safe place to put your money”—has fallen to the edge of junk territory because it decided to build a hockey rink. Every other borrowing the city does—for roads, for sewers, for schools—now costs more because of a building with four ice rinks and a scoreboard.

Revenue Bonds, Explained Through a Stadium Bond Default

If there is one lesson from this stadium bond default, it is this: a revenue bond is only as good as the revenue. That sounds obvious. It is obvious. But it is a truth that gets forgotten every time someone builds a shiny new facility and projects $20 million a year in income.

General obligation bonds rely on a government’s taxing power. If the city needs more money, it can raise taxes. Revenue bonds are different. They rely on a specific stream of income—in this case, ice rink revenue. If the rink makes money, the bonds get paid. If the rink doesn’t make money, the bonds don’t get paid. There is no backstop. There is no safety net. There is no one else’s wallet to reach into.

Except, of course, there was. Maryland Heights has now spent over $1.8 million in backstop payments and $12 million to help finish construction. The city council plans to appropriate another $1 million by mid-April to replenish the reserve fund. The ice rink that was supposed to pay for itself is, instead, being paid for by the taxpayers of a St. Louis suburb.

Eighteen Dollars

The Centene Community Ice Center still stands. The Blues still practice there. Lindenwood’s hockey team still plays there. OVG360, the Oak View Group division that took over management after the city terminated its agreement with the Legacy Ice Foundation, is still trying to make the numbers work. The 4,500-seat amphitheater next door still books concerts.

But the numbers in this stadium bond default, so far, have not worked. The revenue fund is at zero. Officials have raided the reserve fund. The subordinate bondholders are in default. And somewhere in a filing on the MSRB’s EMMA website, there is a material event notice that tells the whole story in a single data point: $45.1 million in outstanding principal, and a revenue account with nothing in it.

Municipal bond investors who own this paper—or paper like it, exposed to the same kind of stadium bond default risk—should be watching the mid-April City Council vote, the next EMMA disclosure, and the facility’s revenue trends under OVG360 management. But they should also be asking themselves a more fundamental question, the one Maryland Heights should have asked in 2018 when a city of 27,000 people decided to borrow $55.7 million to build a hockey palace:

What happens when the ice melts?

Track this bond on MuniBonds.ai: munibonds.ai/bonds/574069AD2

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Municipal bond investors should conduct their own due diligence and consult qualified financial advisors before making investment decisions.