The Bronx Blinked – The Yankees came. The fans came. The cars did not.

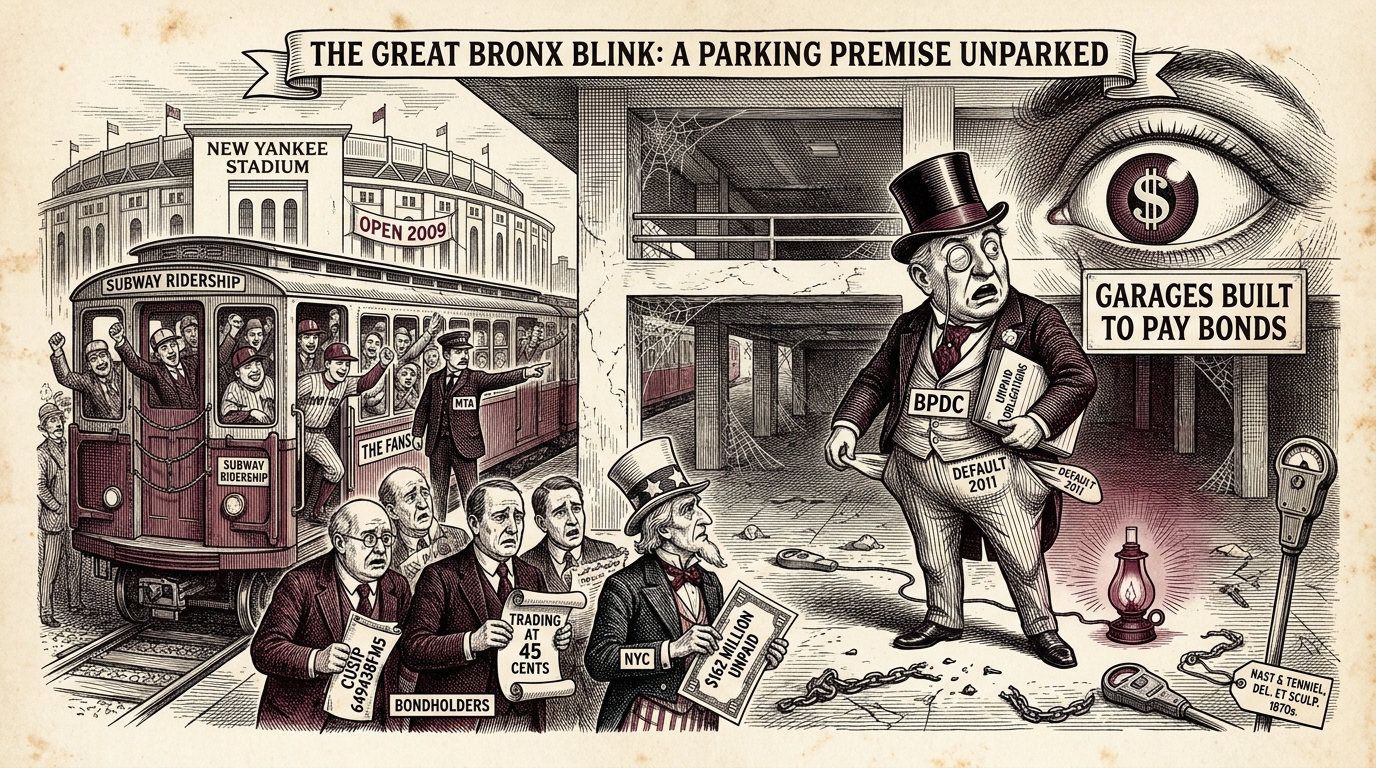

The Yankees came. The fans came. The cars did not…. New York City sold bonds in 2007 based on a simple idea. The new Yankee Stadium would open in 2009 with 81 home games a season. Thousands of fans, 9,300 parking spaces, daily ticket revenue covering debt service.

That was the thesis behind Bronx Parking Development Company (BPDC), an entity created by the New York City Industrial Development Agency to issue revenue bonds backed solely by parking. The structure was straightforward by 2007 standards: a non-recourse special-purpose obligor, three garages built around the new stadium, and projected ridership numbers that assumed Yankees fans would drive to games at roughly the same rate fans drove to the old stadium across the street.

They didn’t. Subway use to Yankees games rose materially through the 2010s. Ride-share ate further into the parking premise after 2013. Bronx Parking Development Company defaulted in 2011 and has not made a payment since.

What happened next was a long American story about a non-recourse obligor that nobody could fix and nobody could let go. Restructuring concepts came and went, including redevelopment ideas tied to a soccer stadium. None of them turned into a payment to bondholders. The garages mostly remained what they had become: a very expensive answer to a question nobody was asking.

By 2022, the City put the situation in writing

Unpaid obligations to New York City topped $162 million by 2022 (per the City counsel’s declaration filed in the BPDC matter). The City was direct: BPDC could not cure the default because there was not enough parking revenue to cover it. The garages built to pay the bonds could not park enough cars to pay the bonds.

This was, in a sense, settled fact. The bonds (CUSIP 649438FM5) carried no rating, traded sporadically, and lived on dealer runs as a quote rather than as a price. For months, the offer level sat around $66 to $67.

Read the latest Munibonds.ai research report on the Yankee Stadium Parking Garage Bonds and our

Three trades, $45 area

Three trades today on CUSIP 649438FM5 (EMMA, May 3 2026). 200,000 par each. The prices: $44.81, $45.06, and $45.19. That is not noise. That is a market clearing.

Unrated bonds do this regularly. It is part of the structural reality of the muni market that funds holding non-rated revenue paper carry quotes for months, sometimes years, that do not reflect the price at which the paper would actually trade if forced to clear. The trade happens to be a clean example because the underlying facts are public, the obligor has been silent for fifteen years, and the prior level was a maintained quote rather than a recent print.

What gives the trade its weight

What gives the BPDC tape its weight is that the structural facts have not changed. The garages still stand. The Yankees still play 81 home games. Bondholders still hold paper that has been in default for fifteen years. The 2022 City counsel filing has been on the record for three years. None of that is news. What is news is the price.

A few observations worth sitting with.

First, the pricing of unrated muni bonds is not a background detail. It is the central fact about the position.

Second, the BPDC story is a useful reminder that the word “unrated” is doing more lifting in muni portfolios than the label suggests. The bond does not carry a rating because the obligor has been in default for fifteen years. Other unrated bonds in the same portfolio may be unrated for entirely different reasons (recently issued, ratings withdrawn, custodian feed gap, never rated to begin with). A community bank, a trust company, or a fund running a thousand-bond portfolio has to distinguish between these, because they imply very different things about what is actually in the portfolio.

Third, the price is the price. The market took fifteen years to clear three small lots, and it cleared them at a level that is not far off from where the obligor’s long-term economics suggest the paper should sit. The House That Ruth Built still stands. The house built for parking, meanwhile, has one remaining question: where exactly is Derek Jeter supposed to park his Lambo?