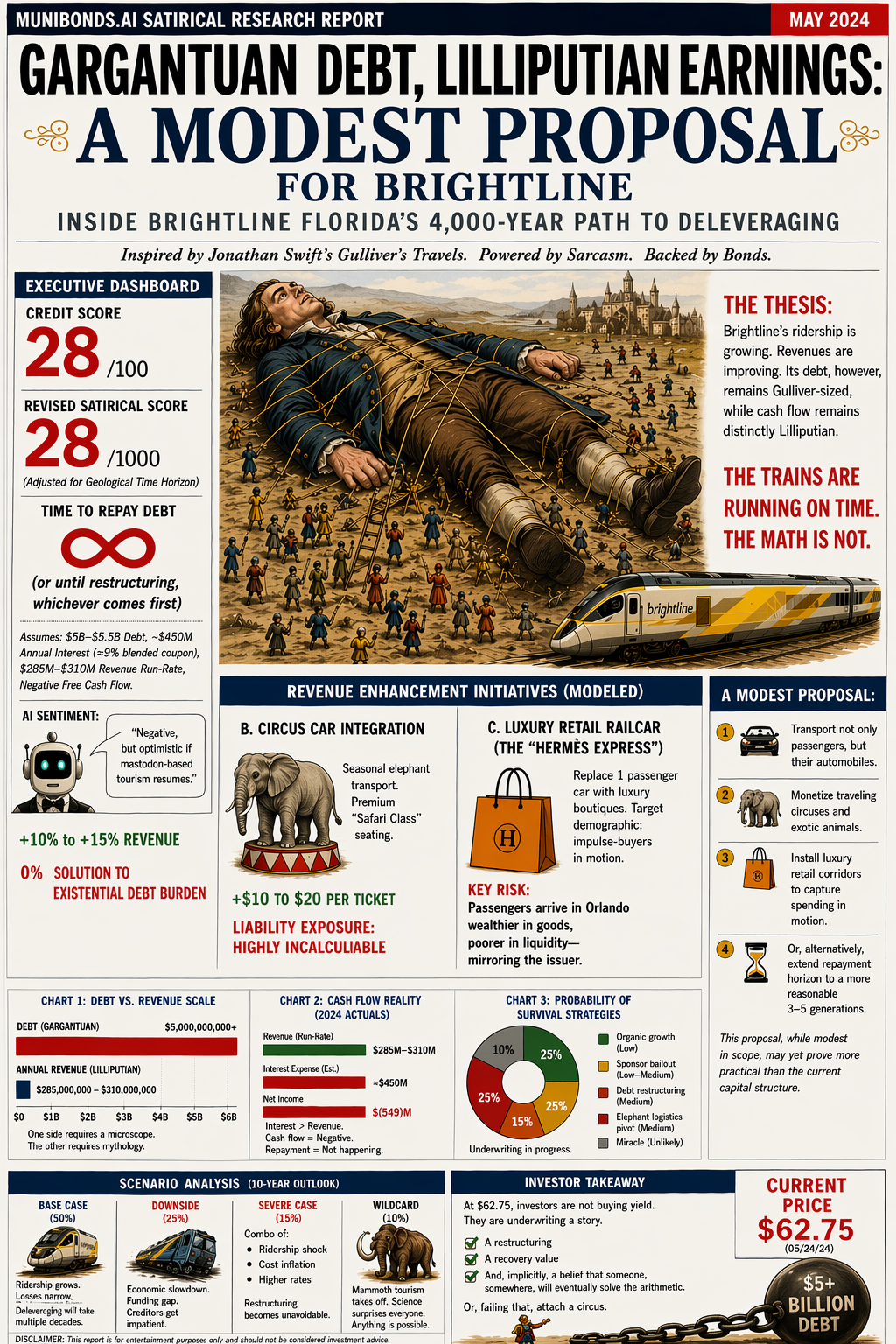

Gargantuan Debt, Lilliputian Earnings: A Modest Proposal for Brightline

Brightline bonds keep raising eyebrows in the muni market.

I rode the Brightline train. The stations are clean. The train is comfortable. It leaves on time. For part of the trip, the view out the window even feels a little like Europe, sort of.

But the finances tell a different story. Brightline has about $5 billion to $5.5 billion of debt. It is bringing in real money—more than $23 million in March 2026 alone—and more people are riding it. But it still lost about $549 million in 2024. The trains are almost full, but the math still doesn’t work.

A Modest Adjustment

A modest proposal for the Brightline Train.

A Modest Adjustment

So what can Brightline do? Perhaps once a year, when the circus comes to town, Brightline could add a special train car for lions, tigers, and bears. It would match the drama of the whole situation and maybe bring in a little extra money. But in the end, elephants and donkeys will probably carry the debt.

The real fixes are less entertaining: restructure the debt, extend the deadlines, talk to creditors and bond insurers, and hope the sponsors help. Those are probably the only real options.

The Real Problem

The problem is not the train itself. The trains run. People ride them. Revenue grows.

The problem is the debt. The company owes so much money that even better ridership and better revenue may not be enough. That is why this story is really about whether the business can ever catch up to what it owes.

Strange But True

Brightline also has a rough safety record, with car collisions, suicides, and even the occasional machine-on-machine violence—like the delivery robot that got pummeled on the tracks. An autonomous Coco food delivery bot recently got stuck on the Brightline tracks.

Read the latest Munibonds.ai report on Brightline bonds

Listen to the latest Munibonds.ai podcast on Brightline Bonds :